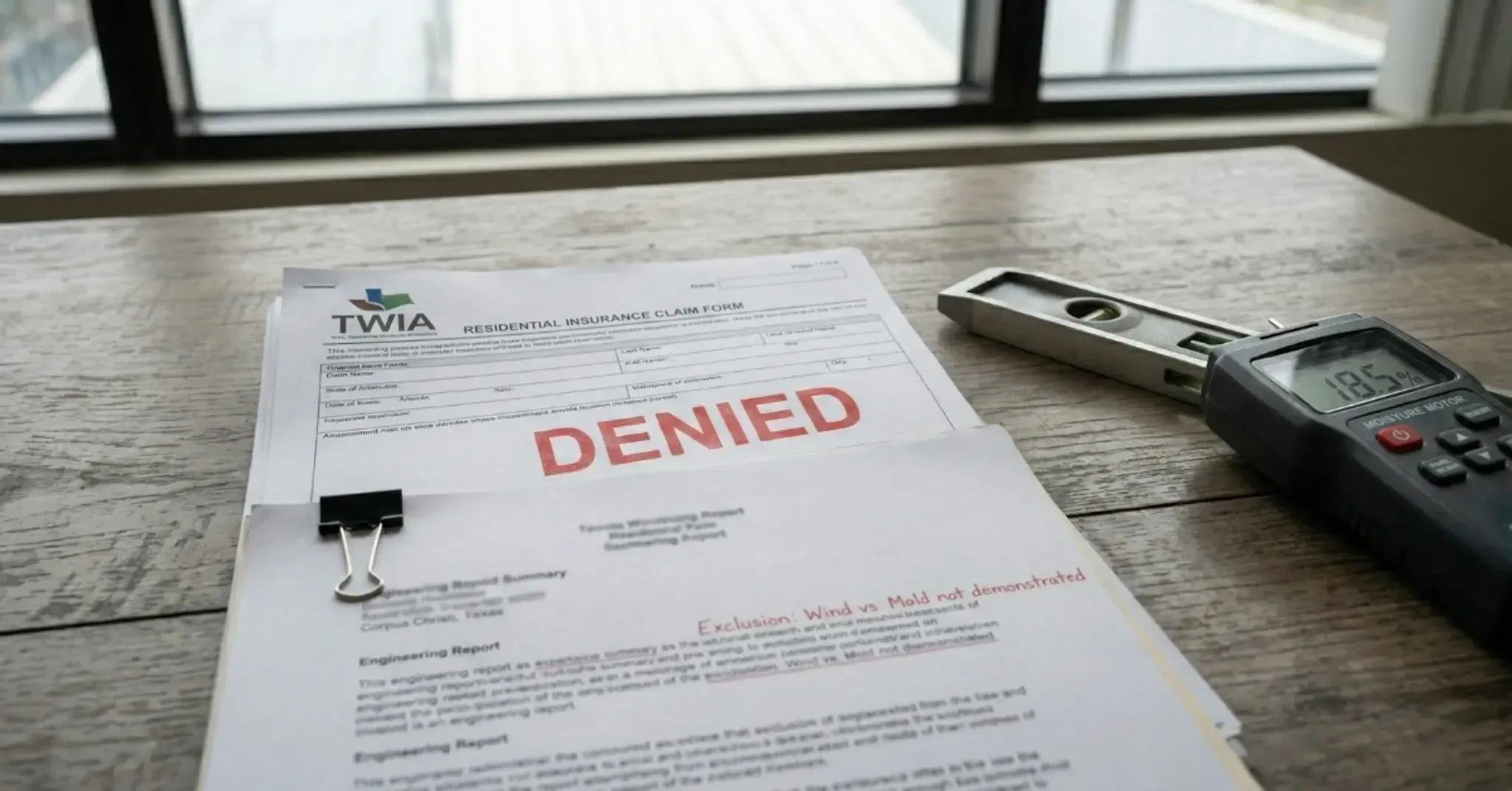

The Texas Windstorm Insurance Association covers wind and wind-driven rain. It does not cover flood water.

When mold shows up after a storm, TWIA adjusters often deny the claim by saying the water that caused it was flood water, not wind-driven rain. The mold is not in dispute. The water source is.

That distinction is where the claim lives or dies. A mold report that shows where the water entered and how it traveled is often the only thing that changes the outcome. Mold testing in Corpus Christi runs about $500 to $800 (more for extensive inspections), and Fast Mold Testing offers transparent published pricing with results in 1 to 2 business days.

How TWIA Decides What It Covers

TWIA is the insurer of last resort for windstorm coverage along the Texas coast. Most Corpus Christi homeowners cannot get windstorm coverage anywhere else, which makes TWIA's decisions final in a way that other insurers are not.

The TWIA policy covers direct loss from wind and wind-driven rain. It excludes loss caused by flood, storm surge, and rising water. When a hurricane or tropical storm hits, both wind and flood often damage the same home.

TWIA pays for what wind did. The National Flood Insurance Program pays for what flood did. The split sounds clean. It rarely is.

The TWIA claims process gives homeowners a path to file and dispute denials.

The problem is that the burden of proof sits with the homeowner once TWIA issues a denial. You have to show why their decision is wrong.

Why Mold Claims Are Especially Vulnerable to Wind-Flood Denials

Mold grows where water was. After a storm, water came from somewhere. TWIA adjusters know that a denial based on flood origin is hard to disprove without solid paperwork.

Mold in a home's lower walls, near the foundation, or at floor level reads as rising water. TWIA denies.

Mold in upper walls, near window frames, at roof vents and seams, or along the underside of the roof decking reads as wind-driven rain. TWIA has a harder time denying that.

The location of the mold relative to the building structure is the argument. An adjuster eyeballing a wet wall cannot make that call with care. A mold inspector who maps the growth pattern, tracks the moisture path from high to low, and names the species can make the case that the water came from above, not below.

What a Mold Source Report Documents

A thorough mold check for a TWIA dispute shows more than whether mold is present. It records where each growth site is located: the height above floor level, the closeness to windows, vents, and roof seams, and the direction of moisture spread behind the surface.

Moisture readings tell a story too. Water that entered through a failed window seal or wind-driven rain through a soffit vent moves differently than flood water rising from the floor. Moisture meters track that path inside the wall. A trained inspector reads the pattern.

The report also names the mold species. Some molds grow fast in outdoor-exposed conditions with salt air and wet wood. Others are linked to long-term indoor dampness. Species data adds weight to a water-origin argument, though it is not proof on its own.

Location, moisture path, and species together are what a TWIA dispute reviewer reads. Fast Mold Testing Corpus Christi produces the kind of lab-backed report that gives the dispute something concrete to work with.

What to Do After a TWIA Denial

TWIA denials can be disputed through the review process or through the Texas Department of Insurance. Neither path is quick. Both benefit from paperwork you commission before cleanup starts.

The first step after a denial: do not clean up. Once the mold is removed, the evidence is gone. An adjuster or appraiser reviewing a clean space has no way to confirm what was there or where it was located. File the dispute first, get the mold report while the damage is still visible, then clean up.

The second step: request the full denial letter with the specific reason. "Flood origin" is a defensible denial. "Pre-existing condition" is a different argument that needs different paperwork. Know exactly what they are claiming before you build a response.

The third step: get an independent mold assessment. Not from a contractor who also wants to sell you the cleanup.

From a firm whose only job is to document what is there and where it came from. That separation matters in a dispute. An adjuster reviewing a report from an inspector with no stake in the cleanup gives it more weight.

Frequently Asked Questions

Can I dispute a TWIA denial on my own?

Yes. TWIA's dispute process is open to homeowners without a lawyer or public adjuster. The appraisal process requires you to hire an appraiser, but the initial dispute does not. A written mold report is the most useful document to have when you start that process.

What if I already cleaned up the mold before filing the dispute?

If cleanup happened before records were made, the dispute is harder but not impossible. Photos taken right after the storm, contractor notes from the repair, and any original TWIA adjuster report can support the timeline. The missing piece is the detailed location and moisture data that a post-cleanup check cannot recover.

Does a public adjuster help with TWIA mold denials?

Public adjusters who work TWIA claims understand the wind-vs-flood argument and know how to build the file. They work on a cut of the claim payout. If the mold claim is large enough, a public adjuster and an independent mold report together are a strong combination.

How long do I have to dispute a TWIA denial?

TWIA claims are subject to Texas's two-year filing deadline for insurance fights. But the stronger your records are at the time of dispute, the better. Waiting means memories fade and damage evidence disappears. File as soon as you have the mold report in hand.

The Denial Is Not the End of the Argument

TWIA denials are common and often wrong. The wind-vs-flood decision is a judgment call the adjuster makes with limited information. A mold source report gives the dispute reviewer better information and a different basis for the decision.

Corpus Christi homeowners who accept the first denial without records leave money on the table. Book an assessment through Fast Mold Testing Corpus Christi before you clean anything up and give the dispute a real base to stand on.

Frequently Asked Questions

- Why does TWIA deny so many mold claims in Corpus Christi, and how can I fight a denial?

- TWIA denies Corpus Christi mold claims most often when adjusters cannot confirm that water entered from a covered wind or storm event rather than from pre-existing moisture or maintenance neglect. A licensed mold assessment that documents the moisture source and timeline gives you the strongest basis to appeal a denial.

- What evidence do I need to prove my Corpus Christi mold claim was caused by a covered storm event?

- To prove your Corpus Christi TWIA mold claim, you need photos of the storm damage entry point, a moisture reading timeline showing when water infiltration began, and a mold lab report that places the growth after the storm date. Fast Mold Testing can provide all three components in a single inspection report.

- How much does a mold inspection cost in Corpus Christi for a TWIA insurance dispute?

- Mold inspections for TWIA disputes in Corpus Christi cost between $500 and $800 (more for extensive inspections). Fast Mold Testing offers transparent published pricing with results in 1 to 2 business days. The report is formatted to support insurance documentation, with moisture source mapping and lab sample results that adjusters and appraisers can use directly.

- How quickly do I need to get a mold inspection after storm damage in Corpus Christi to protect my TWIA claim?

- You should get a mold inspection within the first week after storm damage in Corpus Christi. TWIA adjusters look for evidence that damage was reported and documented promptly. Mold that is allowed to spread without documentation makes it easier for the insurer to argue the damage resulted from neglect rather than the covered storm event.